》Check SMM's cobalt and lithium product quotes, data, and market analysis

》Subscribe to view historical price trends of SMM's cobalt and lithium product spot cargo

SMM News on July 9:

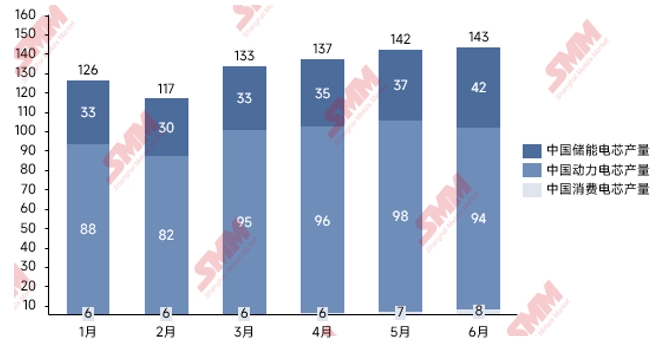

From January to February 2025, influenced by the Chinese New Year holiday, the end-use market demand showed weakness, and the production schedule of battery cells remained at a low level. After entering March, the market gradually recovered, with battery cell production increasing by 14.3% MoM, showing signs of recovery. However, from April to May, due to the lagging effect of the price increase in anode materials in the earlier period, the growth rate of production schedules for lithium battery companies slowed down. In June, affected by unfavourable factors such as the cancellation of the mandatory energy storage allocation policy, the growth rate of production schedules for battery cells further narrowed.Overall, the growth rate of battery cell development in Q1 2025 fell short of expectations.

Chart: SMM's Monthly Production of Lithium Batteries in China from January to June 2025 (Unit: GWh)

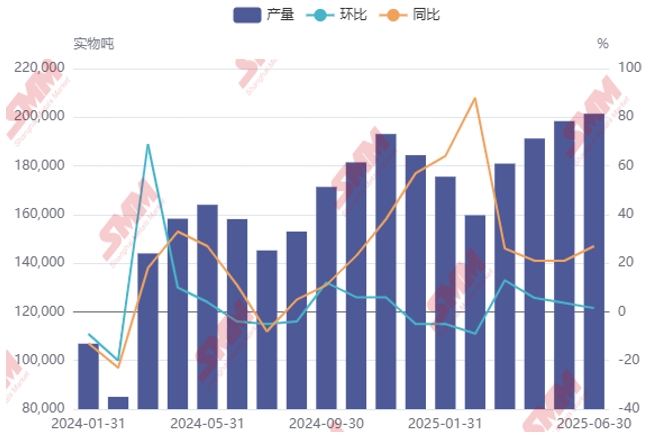

According to SMM statistics, in H1 2025, China'sgraphite anode material production reached 1.107 million mt, showing a YoY increase of36%. At the beginning of the year, affected by the sharp rise in costs and significant compression of profit margins, the production enthusiasm of anode companies was once low; however, as cost pressures eased, uncertainties such as international trade relations followed, leading to the growth rate of production schedules for upstream and downstream of the supply chain falling short of expectations, posing new challenges to the industry's recovery.

In H1 2025, China'sartificial graphite anode production reached 1.01 million mt, showing a YoY increase of36%, accounting for91.2% of the total graphite anode production.

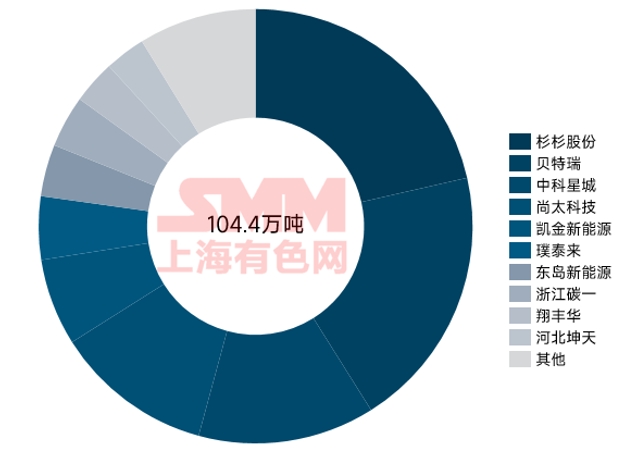

It is worth noting thatShanshan Co., Ltd. also maintained its top position in artificial graphite anode production in 2024, with a market share of approximately 21%.

Chart: SMM's Production of Anode Materials in China from 2024 to 2025 (Unit: 10,000 mt)

In H1 2025,Shanshan Technology performed outstandingly in the artificial graphite field, with shipments ranking at the forefront of the industry, accounting for 21% of the total anode industry shipments. BTR closely followed, maintaining a strong momentum in artificial graphite shipments. Facing industry dynamics,Hunan Zhongke Shinzoom Co., Ltd., Shangtai Technology, and Kaijin New Energy accurately grasped market trends and significantly improved their market shares compared to the same period last year by reasonably adjusting production plans and shipment rhythms. It is worth noting thatJiangxi Zichen, although experiencing a slight decline in production and sales rankings, has shown an improving trend in its overall anode business and achieved steady improvement in operational quality through optimizing and adjusting its customer base.

Chart: Shipments of Artificial Graphite Anode Material in China in H1 2025 (Unit: 10,000 mt)

In summary, the anode material market in H1 2025 was deeply mired in multiple challenges. Under the dual constraints of continuously narrowing profit margins and insufficient growth momentum in end-use demand, both industry production and shipments fell short of expected levels. Looking ahead to H2, with the approaching peak consumption season for downstream NEVs and the gradual release of installations in ESS projects, the demand side for anode materials is expected to see substantial improvement. On the cost side, the temporary factors that previously drove up raw material prices have gradually faded away, and the prices of core raw materials such as low-sulphur petroleum coke and needle coke have returned to rational ranges, which will alleviate cost pressure for anode material producers. Against this backdrop, the profit elasticity of producers is expected to recover, and the industry's profitability space is projected to gradually expand. Combining the dual benefits of recovering demand and cost optimization, the anode material market in H2 2025 is expected to break away from the sluggish pattern of the first half, and the overall development space of the industry is worth looking forward to.

SMM New Energy Research Team

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lv Yanlin 021-20707875

Zhou Zhicheng 021-51666711

Zhang Haohan 021-51666752

Wang Zihan 021-51666914

Wang Jie 021-51595902

Xu Yang 021-51666760

Xu Mengqi 021-20707868